The container shipping industry is facing its most volatile period since the pandemic, as the Persian Gulf conflict triggers a "massive volatility" in spot freight rates that has created a staggering disparity between what different shippers pay for the same route.

While headline indices show moderate week-on-week gains, industry insiders reveal a hidden market reality: some Asia-Europe customers are already staring down $4,000 per 40ft container rates—or higher—even as average indices hover near $2,400.

The Data Disconnect

This week's numbers tell a story of market fragmentation. Drewry's World Container Index (WCI) recorded a sharp 19% spike on the Shanghai-Rotterdam leg, pushing rates to $2,443 per 40ft. Yet Xeneta's XSI index for the same Far East-North Europe trade showed only a 2% increase to $2,345 per 40ft.

"The spread for what customers are actually paying their forwarders and carriers is opening up massively," warned Peter Sand, Xeneta's chief analyst, in an exclusive preview of next week's Loadstar Podcast. "Some of our Far East-North Europe customers are looking at $4,000 per 40ft in a few days, if not already".

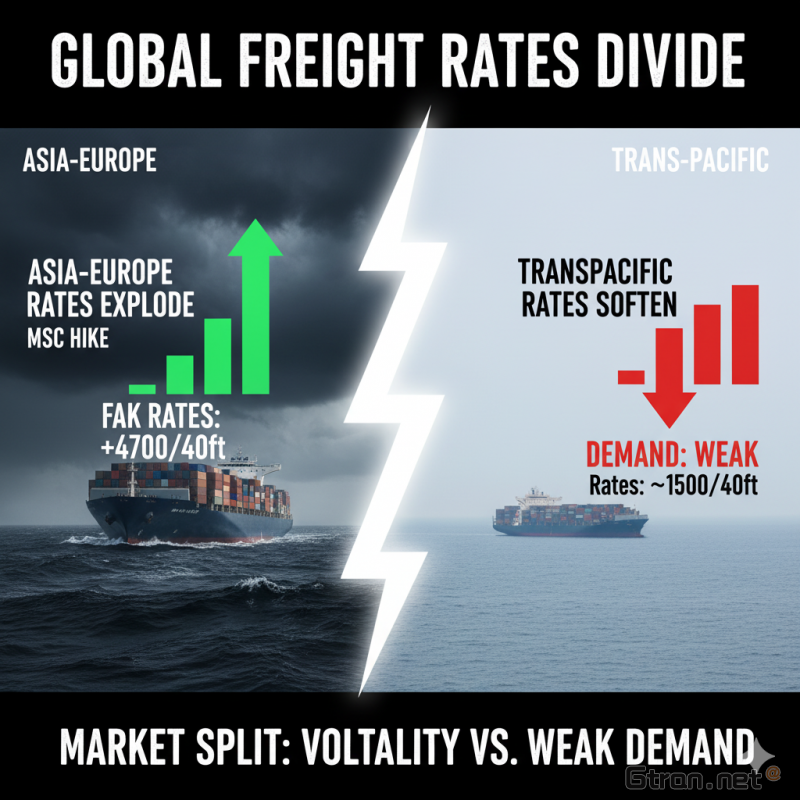

Carrier Offensive: The $4,700 Question

Shipping lines have wasted no time weaponizing the crisis. Mediterranean Shipping Company (MSC)—the world's largest carrier—initially announced a $4,000 per 40ft FAK rate for March 15, only to escalate it to $4,700 effective March 22.

CMA CGM and Hapag-Lloyd have similarly positioned $4,000 per 40ft rates for North Europe, while CMA CGM's Asia-Mediterranean pricing has hit $5,600 per 40ft for March 15, jumping to $6,700 by March 22 .

But here's the catch: forwarders report these hikes are already being discounted in the spot market.

"For Far East westbound, we saw the initial rate increases of around $4,000 come through for the second half of March—however, these are adjusting lower than initially published," one forwarder told The Loadstar, confirming no loading delays or space shortages despite the crisis rhetoric.

The Hidden Tax: Emergency Bunker Surcharges

While base rates fluctuate, one cost is non-negotiable: emergency bunker fuel surcharges. Forwarders confirm these fees are being applied "on top of all NAC/FAK agreements," ensuring shippers face materially higher costs regardless of headline rate negotiations.

Transpacific: The Calm Before the Storm?

Remarkably, the transpacific trades remain operationally insulated from Persian Gulf disruptions—for now. The WCI's Shanghai-Los Angeles route rose just 4% to $2,503 per 40ft, while Shanghai-New York gained 3% to $3,080.

But demand weakness is crushing rates on the US West Coast. Xeneta data shows the Far East-US west coast route actually contracted 5% week-on-week to $1,985 per 40ft, with Freight Right confirming "real" forwarder-paid rates as low as $1,500 per 40ft to the USWC and $2,400-$2,500 to the east coast .

"Demand into the US is really weak at the moment, so that's keeping a lid on transpacific rates," Sand explained .

Stranded Assets: The Hormuz Bottleneck

The crisis has trapped approximately 100 container vessels in the Persian Gulf—representing up to 10% of effective global capacity—with the Strait of Hormuz handling 2-3% of world container volumes. Hapag-Lloyd alone has roughly 150 seafarers stranded on ships in the region, with one company vessel struck by unknown fragments near Jebel Ali last week.

Morningstar has labeled the Iran war "the biggest threat to global shipping and supply chains since COVID," noting that the longer the conflict continues, the more broadly disruptions will be felt across non-Gulf lanes.

Strategic Implications

Industry analysts warn that the current volatility exposes a fundamental shift in carrier-shipper dynamics. With rates varying by as much as $2,000 per container between similarly situated shippers, contract negotiation strategies are being rewritten in real-time.

As one logistics executive noted: "This isn't just about geography anymore—it's about who has the data, the flexibility, and the stomach to navigate a market where the price you pay depends on when you booked, who you know, and how well you can read a geopolitical flashpoint."

Market Outlook: With Ramadan approaching and peak season capacity tightening, analysts expect further divergence between indices and actual transaction prices. For shippers, the message is clear: in this market, the sticker price is just the opening bid.