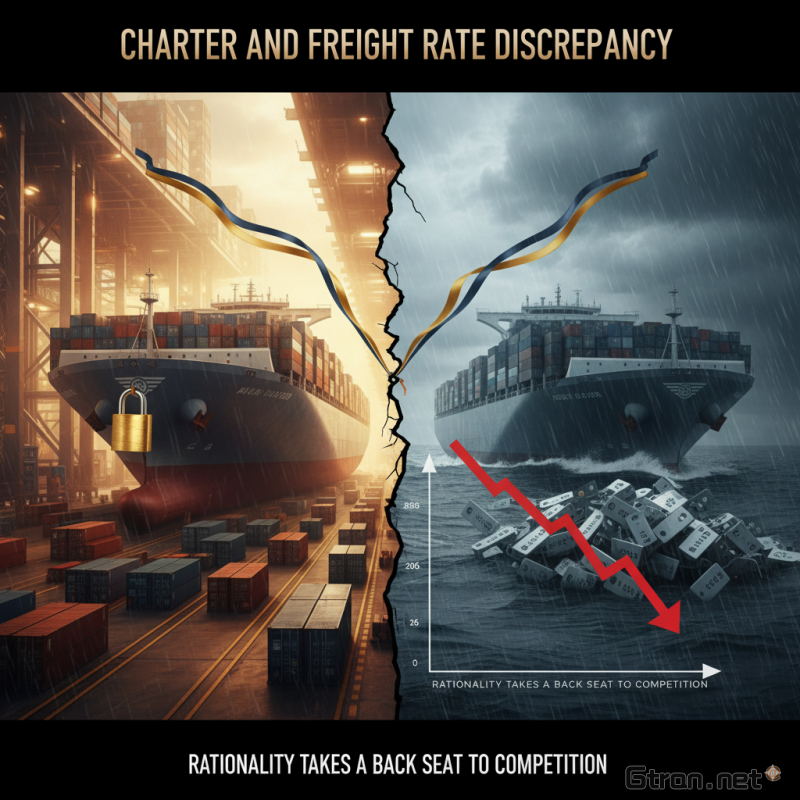

The global container shipping industry appears to be heading into a period where intense competition may overshadow rational decision-making, as evidenced by a growing divergence between charter rates and actual freight rates. Despite a marginal uptick last week, global container freight rates have been on a consistent downward trajectory for the past eleven weeks, signaling an ongoing softening in demand.

This sustained decline in spot freight rates stands in stark contrast to the stubbornly high, albeit slightly easing, charter rates for container vessels. Typically, these two metrics tend to move in closer alignment, as a reduction in freight demand would logically lead to lower vessel demand and, consequently, lower charter costs. However, current market conditions suggest that ocean carriers, having secured lucrative charter agreements during the peak demand periods of the past few years, are now facing the challenge of filling these vessels in a weaker freight market.

Industry analysts are observing that carriers, rather than opting to idle vessels or renegotiate expensive charter contracts, may choose to aggressively pursue market share. This strategy would involve offering highly competitive, and potentially loss-making, freight rates to secure cargo and ensure their chartered ships remain operational. The logic behind this approach, while appearing irrational in the short term, could be to maintain customer relationships, prevent competitors from gaining ground, and position themselves strongly for a potential future market rebound.

Recent news from the shipping sector has highlighted this growing tension. Data from various indices, such as the Shanghai Containerized Freight Index (SCFI) and the Drewry World Container Index, consistently show declining spot rates across major East-West trade lanes. At the same time, reports indicate that while charter rates have seen some softening from their absolute peaks, they remain elevated compared to pre-pandemic levels, trapping many carriers in expensive long-term commitments.

This scenario raises concerns about the potential for a "race to the bottom" in freight pricing, reminiscent of past market downturns where carriers prioritized volume over profitability. Such a competitive environment, driven by the imperative to cover high operational costs tied to charter agreements, could put significant pressure on carriers' margins and potentially lead to further consolidation in the industry. The coming months will reveal whether ocean carriers can navigate this complex landscape with a focus on long-term sustainability, or if the pursuit of market share will indeed take precedence over traditional economic rationality.