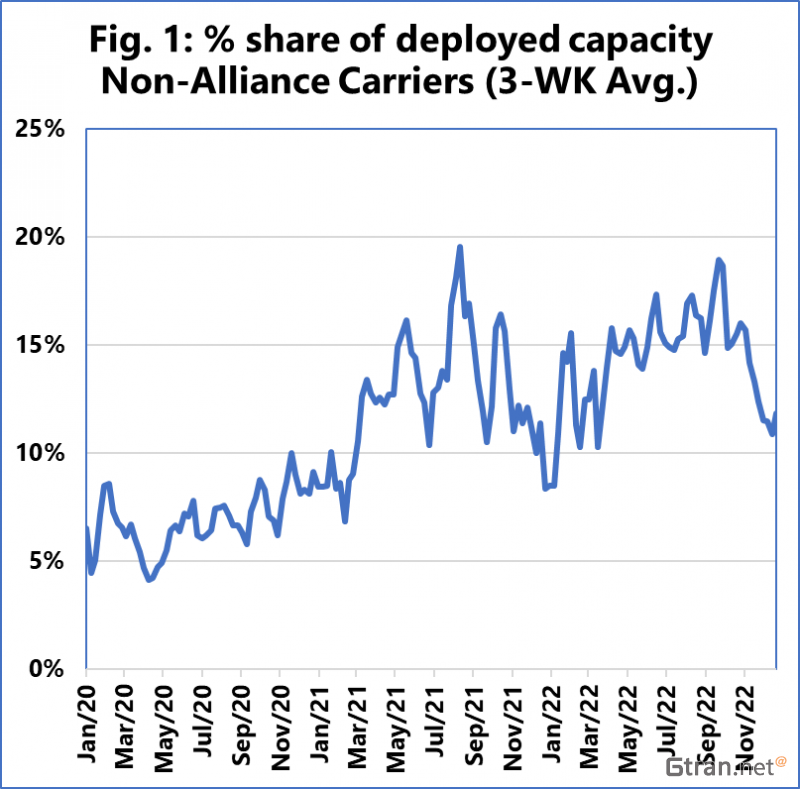

Non-alliance container carriers managed to triple their market share from around 5% to around 15% during the peak of the Transpacific market in the last two years, according to the latest analysis of Sea-Intelligence.

This trend could result from the fact that market conditions were very favourable to carriers from the second half of 2020 until the first half of the current year.

"There was excess demand and a struggle to make enough capacity available to fulfil that demand. This significantly reduces the barriers of entry for smaller carriers who can get in while the market is hot, and then exit when it blows cold. This is exactly what happened, as a large number of newcomers entered the trade," explained the Danish analysts.

Sea-Intelligence's report covers only Pacific carriers that are not members of the alliances, i.e. this analysis does not cover carriers operating under the 2M, Ocean and THE Alliance.

As indicated in the above figure, the market share of these smaller carriers is also set to decline severely as we reach the end of 2022.

Alan Murphy, CEO of Sea-Intelligence, commented, "Much of this additional niche carrier capacity has been sourced from exceptionally high-priced vessel charters for small and inefficient vessels, which in turn has been entirely fuelled by the exceptionally high spot rates, and as these have been coming down fast in recent months, many of these small-vessel services will quickly approach the point where they become loss-making, forcing a swift closure and exit from the market."

This is not unexpected, according to Sea Intelligence, as these small-vessel services were never expected to remain in the market beyond the period of high spot rates.